Today’s AI systems are already highly capable. They can generate content, produce reports, and even participate in price negotiations with suppliers. However, when it comes to the final step—payment—human intervention is still typically required.

Regardless of the AI tool being used, the process often stops at a critical checkpoint: the system completes the selection and decision-making, but still prompts the user to “confirm payment.” This may involve unlocking a device, performing biometric authentication, or entering a password. As a result, while AI improves decision efficiency, it does not close the transaction loop—limiting the full realization of automation.

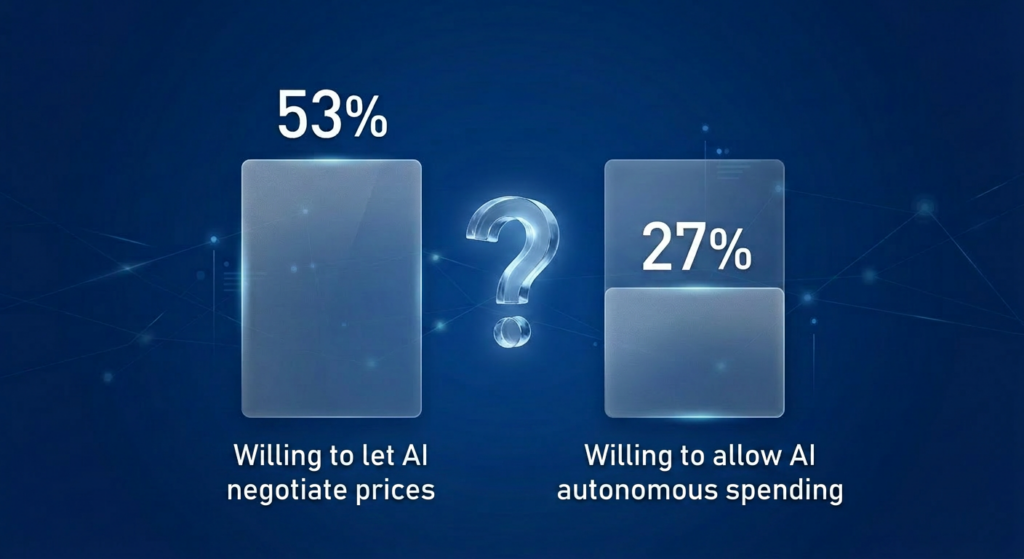

Recent data from Visa highlights this gap: 53% of enterprises are willing to let AI negotiate pricing, but only 27% are comfortable allowing it to execute payments. The 26-percentage-point gap reflects a clear reality—while AI is increasingly trusted in decision-making and execution support, final payment authorization is still largely retained by humans.

In other words, most AI systems today remain at the decision support stage rather than “transaction completion.” The core question is: why can AI decide, but not pay?

| Why Can’t AI Pay on Its Own?**

The limitation stems from a fundamental assumption in existing payment systems: every transaction requires explicit user authorization.

Whether it is card payments, QR code payments, or biometric verification, the core function is to validate both user identity and payment intent. When a transaction is initiated by AI without real-time user confirmation, transaction validity and liability attribution become unclear.

As a result, under the current framework, AI can assist with information filtering and decision-making, but the final act of payment must still be completed by the user.

This leads to a key question:

Is there a mechanism that allows payments to proceed without per-transaction confirmation, while still ensuring that funds are used as intended?

| The AP2 Approach: Predefined Authorization

The Agent Payments Protocol (AP2), introduced by Google in collaboration with over 60 organizations including Mastercard and PayPal, is designed to address this exact challenge.

The core idea behind AP2 is to replace per-transaction confirmation with predefined authorization.

Users can define a clear set of transaction rules in advance, including:

– Budget limits

– Merchant scope

– Time constraints

Within this predefined authorization framework, AI can autonomously complete both decision-making and payment execution—without requiring step-by-step approval.

| How AP2 Works

Consider a familiar scenario:

A user wants to book a flight to Beijing for next Wednesday.

1. User Sets Authorization (Intent Mandate)

The user defines transaction boundaries through a digital authorization:

– Budget capped at 3,000 RMB

– Merchants limited to China Southern Airlines or Air China

– Departure on next Wednesday, with authorization valid within the current week

This authorization acts as both the decision boundary and execution constraint for the AI.

—

2. AI Makes the Decision (Decisioning)

The AI searches and evaluates available options:

– China Southern morning flight: 2,800 RMB

– Air China evening flight: 3,100 RMB

Options exceeding the budget are automatically excluded. Based on timing and constraints, the AI selects the optimal choice.

It then generates a standardized transaction summary (similar to a digital receipt), detailing the flight, price, and merchant.

—

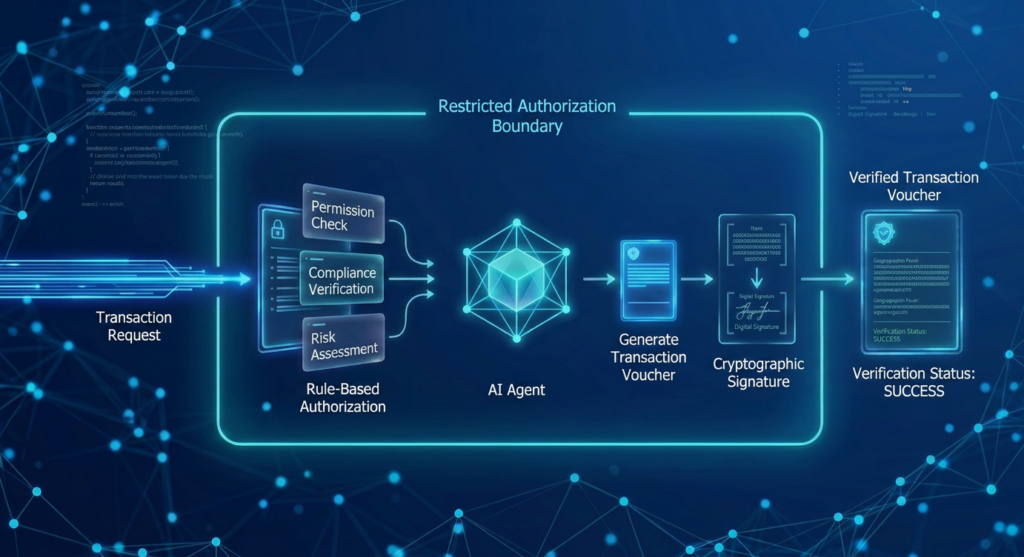

3. Payment Execution (Execution)

The transaction summary is submitted to the payment system for validation:

– Is the amount within budget? ✓

– Is the merchant within the approved list? ✓

– Does the timing meet the constraints? ✓

If all conditions are satisfied, the system proceeds to complete payment and ticket issuance automatically—without requiring further user interaction.

At its core, this model replaces manual confirmation with rule-based validation, enabling controlled automation in payments.

| How This Differs from Traditional Payment Models

AP2 does not replace existing payment instruments (such as cards or digital wallets). Instead, it changes how transaction authorization is handled.

– Traditional model: AI assists with decision-making; the user confirms and executes payment

– AP2 model: Within predefined rules, AI completes both decision and payment execution

Stripe has described the progression of human-to-AI delegation in five stages—from information gathering to full autonomy. Most current applications remain in the early stages, such as form-filling and price alerts.

The key contribution of AP2 is completing the missing layer, payment execution, allowing AI to close the transaction loop within an authorized framework.

| Conclusion

The previously mentioned 26-percentage-point gap ultimately reflects a mismatch between trust in AI decision-making and mechanisms for AI payment authorization.

AP2 introduces a practical framework to bridge this gap: users define rules upfront, and AI executes transactions autonomously within those boundaries without requiring per-transaction confirmation.

As this model matures, transaction scenarios that were previously constrained by manual approval can begin to operate autonomously.

From personal use cases such as travel booking to enterprise procurement, the role of AI in payments is only beginning to take shape, and its potential remains substantial.