For a long time, mobile banking has been widely perceived as a basic tool for checking balances and making local transfers.

However, as global capital flows and cross-border economic activities deepen, user demand for financial services has fundamentally changed. Funds—whether personal or corporate—are no longer confined to a single economy. Scenarios such as receiving local salaries, transferring money across borders, and managing multi-currency assets are becoming the norm, driving financial services toward a more globalized and integrated model.

Our Mobile Banking Platform (MBP) has already been deployed and is running in multiple real-world projects. Current clients include, but are not limited to:

– Asia Digital Bank (digital banking project)

– Silink (cross-border financial services platform)

What these projects have in common is that they serve not just local users, but complex needs spanning multiple countries, currencies, and use cases. It is through these real-world operations that the platform’s capabilities have been continuously validated.

Let’s take a closer look at how these capabilities work in practice through two concrete cases.

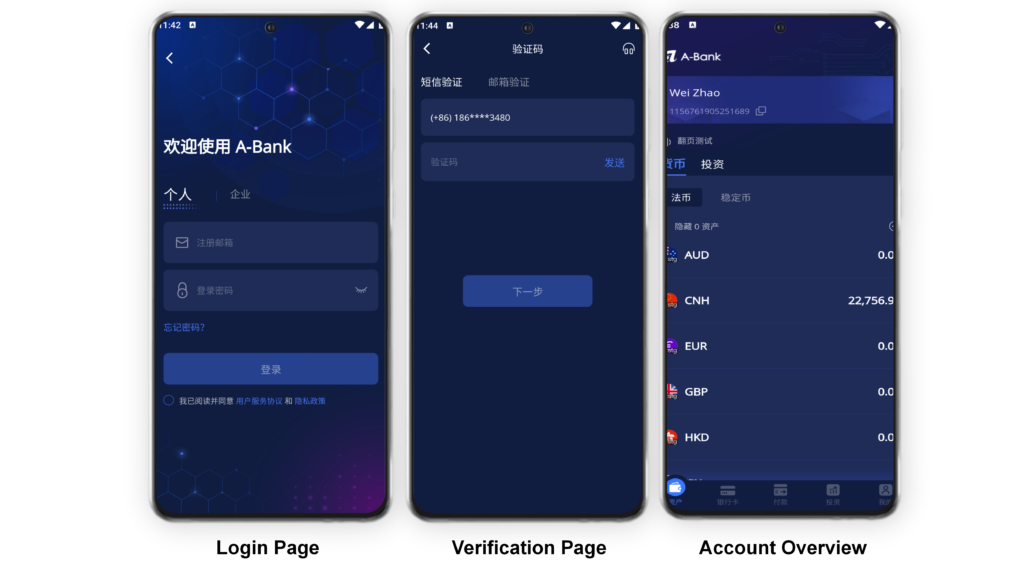

Case 1: Asia Digital Bank — Managing Users Across Multiple Regions

Asia Digital Bank serves users across different countries and regions, each with its own languages, currencies, and regulatory requirements.

Traditionally, the approach has been to build a separate system for each country. This leads to long development cycles, high costs, and the need to start from scratch whenever entering a new market, not to mention inconsistent user experiences.

MBP takes a different approach by integrating all these capabilities into a single system.

Take account opening as an example. Previously, users had to visit a branch, fill out forms, and wait for approval—taking anywhere from a few days to a week. Now, users can complete identity verification and submit documents directly on their mobile devices, finishing e-KYC onboarding within minutes.

Cross-border remittance has also been streamlined. Instead of repeatedly filling in information and manually checking exchange rates, users can now complete transfers and currency exchange in a single flow. Exchange rates can be locked in advance, and fees are displayed upfront—eliminating the need to switch between different systems.

At its core, this means bringing previously fragmented processes and data into a unified system.

Before: One system per country, with disconnected data.

Now: One unified system supporting multi-region operations.

If Asia Digital Bank addresses how a bank serves users across countries, Silink tackles a different challenge:

How do you control and manage funds as they move globally?

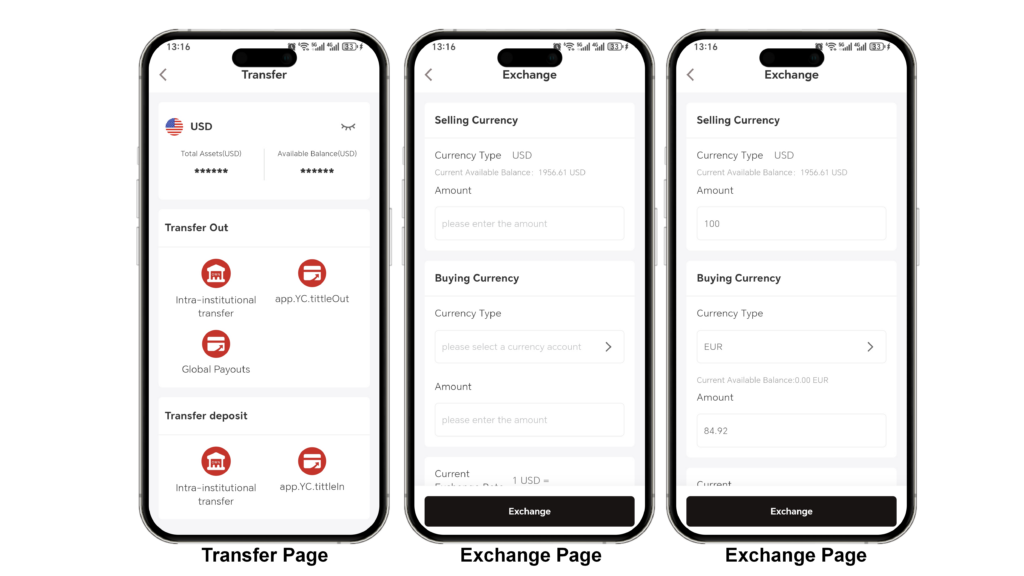

Case 2: Silink — Managing Cross-Border Collections

Silink serves global enterprise clients, where fund flows are more frequent and complex.

The main challenges fall into three areas: fragmented collection channels, volatile exchange rates, and higher risk control requirements. In many companies, the reality is: reconciliation is manual, exchange rates are managed via spreadsheets, and risk control relies heavily on experience.

MBP addresses these issues by consolidating all capabilities into a single system.

In fund processing, remittance and FX conversion are merged into one workflow. Information is entered once, outcomes are determined upfront, and manual errors are reduced.

More importantly, risk control is embedded directly into each transaction step. The system identifies abnormal behavior in real time and blocks suspicious activity immediately, rather than relying on post-event fixes.

Before: Fragmented channels, manual reconciliation, experience-based risk control.

Now: Unified platform with automated calculations and real-time interception.

The two examples above illustrate how the platform works in specific scenarios. If we break down these capabilities, the full picture becomes even clearer.

What Can One Unified System Do?

In the past, building a complete fintech service required integrating multiple vendors—resulting in fragmented systems and long implementation cycles.

MBP consolidates core capabilities into a single system. From onboarding and account management to collections, FX, and cross-border transactions, all key processes are seamlessly connected within one framework.

Some of these capabilities are foundational—without them, the system simply cannot function. Others build on top of this foundation to enhance the overall user experience.

Core Capabilities

Multi-currency Accounts

Manage multiple currencies under a single account. Balances, transaction records, and FX history are all accessible in one interface. Each currency is accounted for separately, providing clear asset visibility, with automated multi-dimensional reports generated at the end of each period.

Global Collections and Cross-border Transfers

Supports multiple inbound channels and one-click cross-border remittance. Exchange rates are transparent and can be locked in advance, with clear fee breakdowns. Transactions comply with local AML/CFT regulations.

Foreign Exchange (FX)

Real-time exchange rates. FX conversion and transfers are completed within a single workflow, without switching pages. All records are traceable.

Once these core capabilities are in place, the foundation for cross-border financial services is established. On top of this, additional features further enhance the user experience.

Extended Capabilities

– Multi-language, multi-timezone onboarding with e-KYC

– Wealth management: subscription, redemption, automatic dividend distribution, and risk-based recommendations

– Financial management: periodic reports, budget alerts, and asset allocation visualization

Together, these create a more complete and seamless user experience.

The capabilities above are visible to users. But for financial products, there is an even more fundamental layer: Security.

Is the Platform Secure?

This is one of the most common concerns among users.

MBP shifts the security perimeter to the client side. While verifying accounts, the system continuously monitors device and environmental conditions. Any anomalies are intercepted in real time.

At the same time, authentication methods dynamically adjust based on the risk level of each operation. Routine actions remain convenient, while high-risk transactions trigger stronger verification.

Security is no longer just a backend function—it is embedded throughout every interaction.

There are two layers of protection:

– The client side monitors device integrity

– The server side analyzes behavior

Together, they coordinate to detect and respond to anomalies. In addition, compliance requirements across different regions are built into the system from the outset.

Why Choose This Solution?

Based on these projects, three key advantages stand out:

True Global Capability

Multi-language, multi-currency, and multi-timezone support are all built into a single system, enabling direct service for users across different countries.

Highly Modular, Fast Deployment

Each capability is modular and can be combined as needed. This shortens integration time, accelerates system launch, and significantly reduces operational costs.

Strong Security + Compliance Architecture

A dual-layer security model—client-side device monitoring and server-side behavior analysis—ensures real-time risk control. Each module includes built-in compliance logic, with full data traceability.

If you are expanding global financial services, you may already be facing practical challenges: system limitations that cannot keep up with business growth, compliance requirements slowing market entry, and increasing complexity in managing multi-currency, multi-region operations.

Gifpay has supported multiple fintech companies and institutions by providing a unified mobile banking platform—enabling them to quickly build cross-border financial capabilities without starting from scratch.

We’re open to further discussions on how to improve your global operational efficiency.